[ad_1]

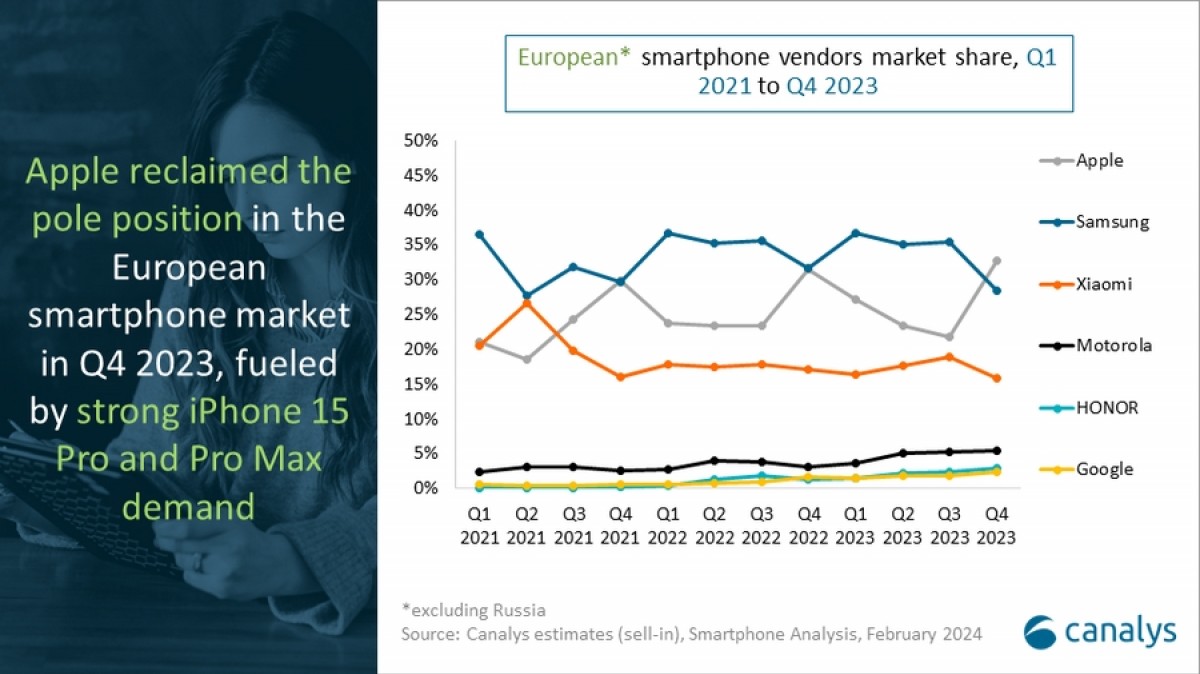

Canalys revealed that Apple turned the best-selling smartphone maker in Europe throughout This fall 2023. The US firm’s success was fueled by robust demand for the iPhone 15 Pro and Pro Max in the course of the vacation interval, however Samsung stored the highest spot for the entire of 2023.

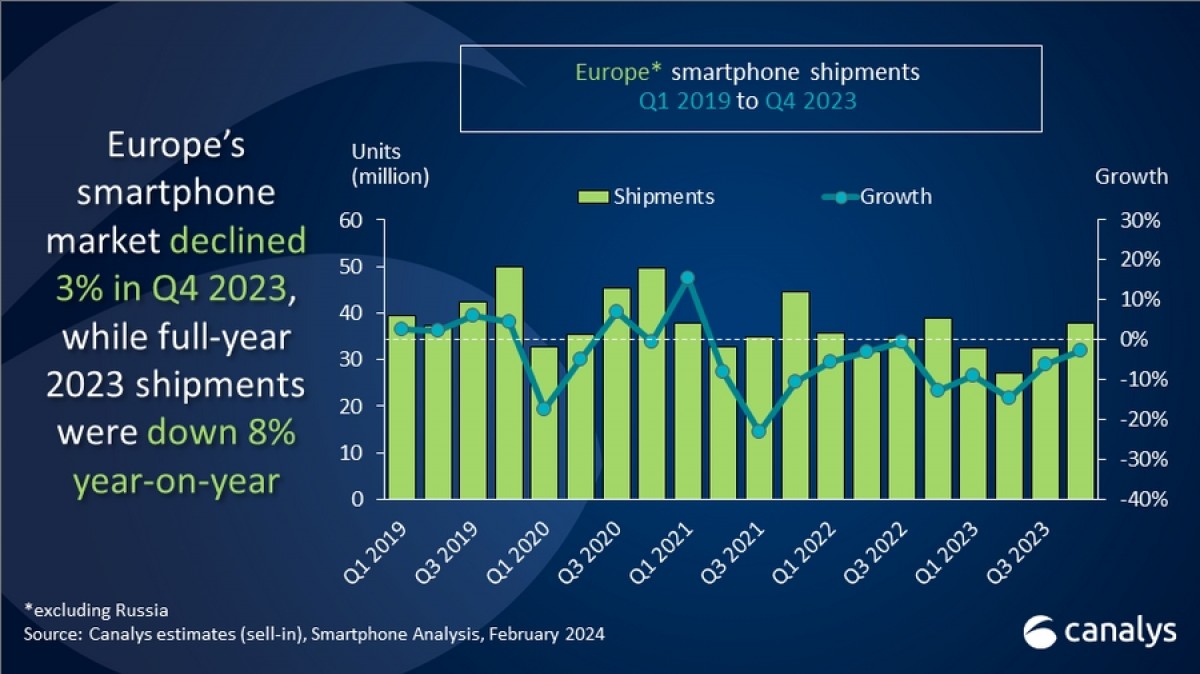

The general market noticed 129.8 million shipments for the calendar yr, which was 8% decrease than the 140.8 million items in 2022. Nevertheless, Canalys predicted that Europe will see a single-digit development subsequent yr, pushed by an impending refresh cycle of units purchased in the course of the pandemic.

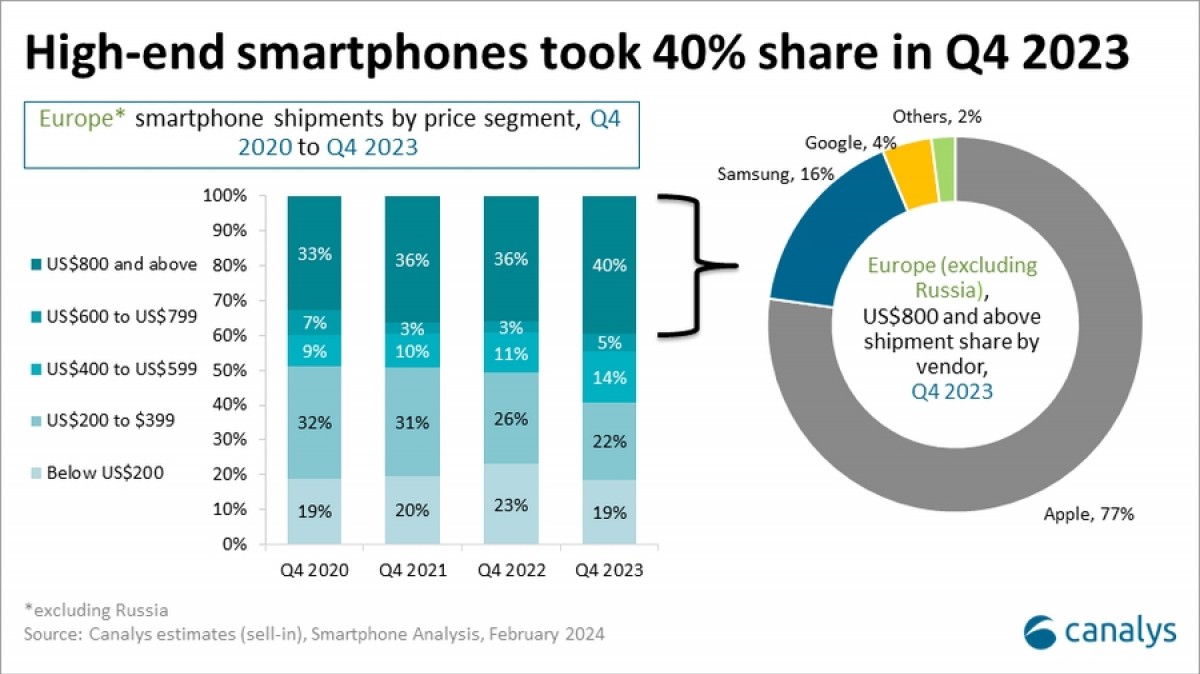

Excessive-end smartphones took a file share of the entire European market in This fall 2023. In accordance with Runar Bjorhovde, Analyst at Canalys, virtually 40% of all shipments have been for telephones that price over $800. Three out of 4 units have been an iPhone, adopted by Samsung with a mere 16% share.

Apple stored a virtually flat quantity of shipments throughout This fall 2023; it’s Samsung and Xiaomi that flopped massively, permitting the US firm to rise on high. The Prime 5 noticed the resurgence of Honor, and Canalys stated we must always count on smaller manufacturers to extend their share within the close to future. This consists of Oppo, which settled with Nokia on 5G patents, permitting the Chinese language maker to reintroduce its units in main European markets.

| Firm | This fall 2023 shipments (in million) |

This fall 2023 market share |

This fall 2022 shipments (in million) |

This fall 2022 market share |

Change |

| Apple | 12.4 | 33% | 12.2 | 31% | 1% |

| Samsung | 10.8 | 28% | 12.3 | 32% | -12% |

| Xiaomi | 6.0 | 16% | 6.6 | 17% | -10% |

| Motorola | 2.0 | 5% | 1.2 | 3% | 73% |

| Honor | 1.1 | 3% | 0.5 | 1% | 116% |

| Others | 5.5 | 15% | 6.1 | 16% | -8% |

| Whole | 37.8 | 100% | 38.9 | 100% | -3% |

Firms would see a rise in shipments provided that they apply a holistic strategy emphasizing innovation, reliability, backend logistics, regulatory compliance, and a transparent model message, added Bjorhovde.

| Firm | 2023 shipments (in million) |

2023 market share |

2022 shipments (in million) |

2022 market share |

Change |

| Samsung | 43.7 | 34% | 48.9 | 35% | -11% |

| Apple | 34.6 | 27% | 36.2 | 26% | -4% |

| Xiaomi | 22.2 | 17% | 24.7 | 18% | -10% |

| Motorola | 6.4 | 5% | 4.7 | 3% | 34% |

| Oppo | 3.7 | 3% | 6.7 | 5% | -45% |

| Others | 19.2 | 15% | 19.6 | 14% | -2% |

| Whole | 129.8 | 100% | 140.8 | 100% | -8% |

In the long term, distributors will improve deal with the on-device consumer expertise with AI on the core, emphasizing personalization, ecosystem interplay, productiveness, and leisure. Nevertheless, investing in AI ought to be adopted by educating customers on maximizing the ability of on-device AI options; in any other case corporations won’t see a robust return on their funding.

[ad_2]

Source link